The Shanghai/Capella Upgrade

Your Ultimate Guide to ETH Staking Withdrawals

All you need to know about the Shanghai/Capella upgrade, and what it means for stakers and the web3 ecosystem.

March 2023

Own a piece of web3 history

The Shanghai/Capella NFT collection celebrates the upgrade, a technological milestone on the Ethereum roadmap that will simultaneously upgrade the blockchain’s execution and consensus layers to enable staked ETH withdrawals.

Executive Summary

Ethereum is undergoing a period of rapid infrastructural development. Since the Ethereum blockchain’s first implementation launched in 2015, it has undergone a series of planned technical upgrades. Each of these upgrades has brought the Ethereum vision further into focus—to be the open, decentralized, credibly neutral, and permissionlessly programmable infrastructure layer upon which the future of the internet, the economy, and much of our digital lives is being built.

In September 2022, The Merge unified Ethereum’s consensys and execution layers. It was a pivotal moment in the history of Ethereum, having delivered a number of important improvements, including the reduction of the network’s carbon footprint by 99.95%. By switching to the Proof of Stake consensys mechanism, the Merge changed the way value accrues across the Ethereum network, and reduced new ETH issuance by a staggering 88%. Prior to the Merge, the introduction of EIP-1559 made Ethereum transactions more efficient by changing Ethereum’s gas fee system from a bidding system, to a system with two components—a standard base fee for each block (which is burned by the protocol), and an optional tip (priority fee) users can pay to speed up their transactions. The Merge, in combination with the EIP-1559 burn rate, has led to the most deflationary moment in Ethereum’s history, and bolstered the network’s security.

Now, the Ethereum community is rallying behind the next planned upgrade on the roadmap—the Shanghai/Capella upgrade. It is doubly named because it is the first simultaneous upgrade of Ethereum’s execution layer and consensys layer, and is highly anticipated because it will enable staked ETH withdrawals.

In particular, the upgrade will enable ETH that is staked on the consensys layer to be withdrawn to an Ethereum execution address for the first time since ETH staking became possible in December 2020.

The activation of withdrawals resolves another ‘unknown’ in the Ethereum roadmap—likely encouraging increased participation by validators, and precipitating further decentralization and security of the Ethereum network. By increasing the portability of stake, withdrawals will lead to increased competition amongst staking providers—likely driving further innovation within the sector, and progressively lowering barriers to entry.

Stakers who utilize third-party staking services will gain the opportunity to (re)evaluate how and where to stake their ETH based on factors such as rewards maximization, validator performance, simplicity of the user experience, and fees.

Solo staking (operating an Ethereum validator independently) brings the most decentralization and security benefit to the network, but remains challenging for most retail stakers due to the associated technical and operational demands. Those who wish to stake without this operational overhead can choose from a number of different offerings, ranging from fully-custodial and centralized providers, to non-custodial, decentralized protocols. Each staker has a responsibility to select a values-aligned partner whom they are confident will preserve the characteristics of Ethereum that the staker values, whatever those may be. Collectively, stakers are the custodians of Ethereum’s values.

The Shanghai/Capella upgrade is expected to be a significant event for Ethereum. It will have several implications for stakers, the Ethereum staking ecosystem, and DeFi more broadly.

Partial and full withdrawals will give long-term stakers access to funds that have been locked for upwards of two years. Early stakers however, have demonstrated their belief in Ethereum, and may be more likely to stake this newfound liquidity, rather than take profits.

By reducing the liquidity risk of staking ETH, withdrawals could inspire confidence in liquid staking protocols and make ETH staking a more attractive opportunity in general, especially for typically risk-averse institutions.

Finally, we expect to see an increased flow of liquid staking tokens into DeFi protocols as both confidence in these tokens, and competition amongst their issuers, builds.

On March 22, we discussed the tangible effects of the Shanghai/Capella upgrade on the Ethereum ecosystem. Watch the on-demand webinar →

Authors

Andrew Breslin, Product R&D

Michiel Milanovic, DeFi Market Analyst

Simran Jagdev, Senior Content Marketing Manager

Contributors

Ben Edgington, Lead Product Owner, Protocol Engineering

Mikhail Kalinin, Lead Researcher, Protocol Engineering

Roberto Saltini, Lead Researcher, Protocol Engineering

Kuhan Tharmananthar, Product Lead, Consensys Staking

Matthieu Saint Olive, Senior Product Manager, Consensys Staking

Abad Mian, Lead Product Manager, MetaMask Staking

Johann Bornman, Group Product Lead, MetaMask Institutional

Matt Nelson, Product Manager, Hyperledger Besu & Web3Signer

Nicole Adarme, Head of Institutional Marketing

Tsvetan Mitev, Senior Graphic Designer

Introduction

Ethereum is the infrastructure layer upon which the future of the internet, the economy, and much of our digital lives are being built. Supporting our digital futures, on a global scale, requires improving Ethereum’s scalability and security while maintaining the decentralization of the network; in other words, solving the blockchain trilemma.

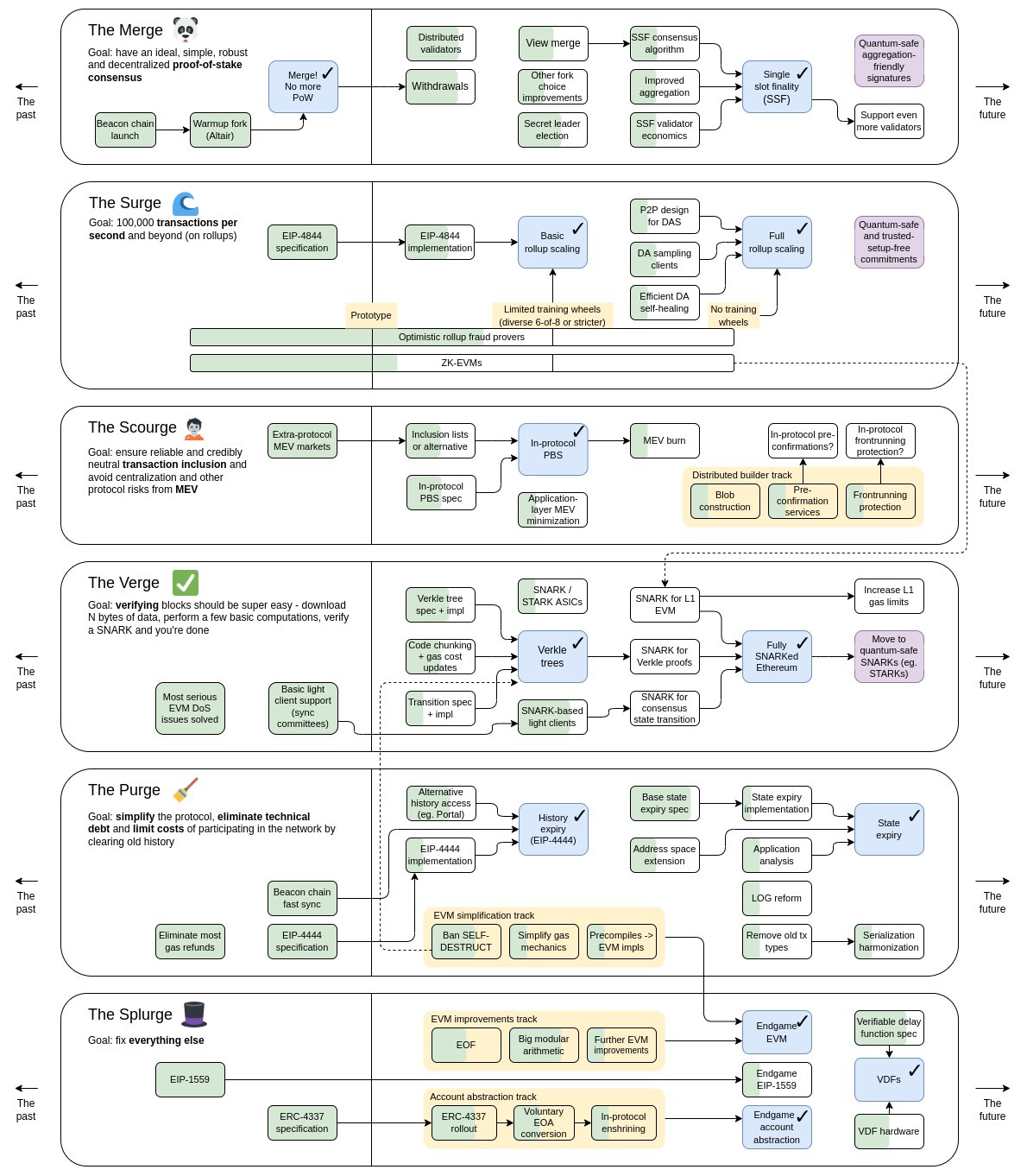

The solution—which is no easy task—is expected to be delivered in six phases: the Merge, the Surge, the Scourge, the Verge, the Purge, and the Splurge. Each phase of Ethereum’s roadmap is largely independent from the others, and is being worked on in parallel.

The most recent upgrade to Ethereum, the Merge, was successfully executed on September 13, 2022. The Merge refers to the joining of Ethereum’s execution layer (EL) and consensys layer (CL), which marked Ethereum’s transition to the Proof of Stake (PoS) consensys mechanism. This move away from the energy-intensive Proof of Work (PoW) consensys mechanism reduced Ethereum’s annualized energy consumption by more than 99%.

Post-Merge Ethereum operates as a single blockchain consisting of two layers: the execution layer is where Ethereum transactions are processed and broadcast to the rest of the network, while the consensys layer runs Ethereum’s PoS consensus algorithm, and handles transaction settlement and finality. According to Vitalik Buterin, this upgrade puts us just over halfway through Ethereum’s broader roadmap.

Figure 1. The Ethereum RoadmapSource: Twitter, Vitalik Buterin

Next up is the Shanghai/Capella upgrade, where the former is the name of the EL upgrade and Capella is the name of the CL upgrade. The key outcome of Shanghai/Capella is that it will enable staked ETH withdrawals.

Stakers that have ETH currently locked on Ethereum’s CL, i.e. validator balances, will be able to withdraw it to an Ethereum execution address. An execution address is simply the standard address on Ethereum mainnet that users are familiar with.

This report aims to situate the Shanghai/Capella upgrade in the broader Ethereum roadmap, and provide an overview of the three key features it enables: updating the withdrawal credential of a validator, partial withdrawals, and full withdrawals.

From here, we’ll dive into the implications of withdrawals. We’ll examine how partial and full withdrawals might impact the liquid supply of ETH, and investigate how the increased portability of stake is driving competition and rapid innovation across Ethereum’s staking industry.

What is the Shanghai/Capella upgrade?

As mentioned above, the next planned upgrade to Ethereum is known as both the Shanghai upgrade, and the Capella upgrade. Shanghai/Capella is doubly named since it is the first simultaneous upgrade of Ethereum’s EL and CL. In principle, upgrading both layers simultaneously is not mandatory, so for precision’s sake, we will use the respective names for the EL and CL upgrades.

As the first simultaneous upgrade to Ethereum’s EL and CL, Shanghai/Capella will also be the first Ethereum fork that will be triggered by a specific timestamp. With the exception of the Merge, all previous forks were triggered by reaching a specific block number. Switching to a fork triggered by a timestamp allows for the EL and CL to be upgraded synchronously.

Apart from withdrawals, the Shanghai/Capella upgrade will also deliver a number of minor technical improvements to the Ethereum Virtual Machine (EVM).

However, since withdrawals, or EIP-4895, are the key feature being delivered in the upgrade, this report will focus on that.

The exact date that the Shanghai/Capella upgrade will go live remains to be determined, but Ethereum Core Devs—who volunteer to contribute to the development of this open-source software—have been making steady progress towards this goal. They have been testing the fork on various testnets, the most recent being the Sepolia testnet, which successfully underwent the Shanghai/Capella upgrade at 4:04 AM UTC on February 28, 2023. This will be followed by the Goerli testnet and, assuming all goes well, the Ethereum mainnet.

Hear from experts on how the Shanghai/Capella upgrade furthers the importance of decentralization and the impacts on retail and institutional users. Watch the on-demand webinar →

Role of Stakers in Ethereum Governance

At its core, Ethereum’s value lies in the decentralized network of validators who collectively build and secure the Ethereum blockchain, and the broader social layer of the Ethereum community. It is this decentralized, permissionless community of contributors that gives rise to Ethereum’s credible neutrality, censorship resistance, openness, immutability, and near-unbreakable security. For this reason, running an Ethereum validator independently, also known as solo staking, is considered the gold standard of Ethereum staking as it confers the greatest benefit to both the staker and the decentralization of the network.

By ensuring that no one entity has disproportionate power over decision making across Ethereum, solo stakers are crucial to the network. A number of communities like ETHStaker, tools like ethdo, and dedicated execution and consensys layer client teams like Besu and Teku, are making running an Ethereum validator independently more accessible for an increasing number of Ethereum community members.

That being said, running a validator independently presents technical, operational, and financial barriers for some users. These types of Ethereum stakers have many options through which they can stake, including non-custodial staking-as-a-service providers like Consensys Staking, and the top liquid staking protocols accessible through MetaMask Staking.

While stakers can delegate the operational aspects of running a validator to a third party, the responsibility to select a values-aligned partner that will preserve the characteristics of Ethereum that the staker values, still lies with them. The choice of where, and with whom, these individuals stake has crucial implications for Ethereum’s decentralization.

Despite being a community-governed system, executing the Ethereum roadmap entails making significant infrastructural changes, and therefore making important decisions. To make these decisions, a robust decentralized governance process is required to reach consensys amongst impacted stakeholders; in other words, every Ethereum community member.

Ethereum governance happens off-chain, meaning that decisions happen through an informal process of social discussion. If the community reaches consensys, the change is implemented in code. Every member of the Ethereum community is involved in Ethereum’s governance process, including stakers of every kind. Stakers are the custodians of the Ethereum network, and by staking independently, or non-custodially allocating their stake to a values-aligned partner, stakers can “vote” with their stake and influence the future direction of Ethereum.

For most Ethereum stakers, the Shanghai/Capella upgrade provides the first opportunity to change how, and with whom, they originally decided to stake. This presents an opportunity for stakers of all kinds to consider their personal values, the values they want Ethereum to embody, and to stake in a way that reflects this. Those with the means to do so, who aim to be self-sovereign and to contribute to Ethereum’s decentralization, should consider running a validator independently. Others can “vote with their stake” through a values-aligned partner. In this way, the Ethereum community as a collective can preserve what makes Ethereum the decentralized trust infrastructure for our global, digital future.

With that in mind, let’s do a deep dive into withdrawals, how they will work, and how their implications will play out across the Ethereum ecosystem after the Shanghai/Capella upgrade.

Learn more about the role of stakers and how they contribute to decentralization, and the health and security of the Ethereum ecosystem. Watch the on-demand webinar →

What are Withdrawals?

We know that the key outcome of the Shanghai/Capella upgrade is to allow stakers to withdraw their staked ETH, but more specifically, it will deliver three key features related to withdrawals:

The ability to update the withdrawal credentials of an Ethereum validator from the older 0x00-type (derived from a BLS key), to the newer 0x01-type (derived from an Ethereum address).

Partial withdrawals, or the periodic and automatic “skimming” of earned, consensys layer rewards from an active validator’s balance (in excess of 32 ETH).

Full withdrawals, or the reclaiming of an “exited” validator’s entire balance.

While partial and full withdrawals are distinct operations, it’s worth briefly noting some commonalities between them.

First, only validators with the newer, 0x01-type withdrawal credentials will be eligible for partial and full withdrawals. Validators with the older, 0x00-type withdrawal credentials can become eligible by updating their credentials to the newer version. However, there is no immediate need to do so, as 0x00-credentialed validators will continue earning rewards like they have since the genesis of the Beacon chain.

Further, there is a single, automated withdrawal process for both partial and full withdrawals. Every 12 seconds (each slot), the protocol “sweeps” through Ethereum’s validator set and identifies the first 16 validators that are eligible for either a partial or a full withdrawal. Up to 16 withdrawals can be processed per slot, however, full withdrawals are processed less quickly as they require first “exiting” the validator, and an additional delay.

Lastly, executing a partial or full withdrawal will have no associated gas costs. While both partial and full withdrawals result in the balance of an Ethereum address being credited with the withdrawn amount, they are not transactions processed by Ethereum’s EL. Rather, withdrawals are considered system-level operations, or account balance top-ups, which work in a similar way to the coinbase transactions paid to miners in PoW blockchains. Since only 16 of these operations are allowed per block, and the cost of executing them is negligible relative to user and smart contract transactions, withdrawals will not incur gas costs.

Updating Withdrawal Credentials

Activating a new Ethereum validator requires depositing 32 ETH, along with a payload of other data, to Ethereum’s deposit contract. Part of this payload of data is a field called the validator’s withdrawal credential, which defines where a validator’s withdrawn balance is sent.

There are currently two versions of withdrawal credentials that an Ethereum validator might have, and they are differentiated by their withdrawal prefix, which is either: the 0x00-type, or the 0x01-type.

Only validators with 0x01-type credentials are eligible to have their balances partially or fully withdrawn. This is due to a technical difference between these withdrawal credential types. Namely, the 0x00 credential is derived from a BLS public key, whereas the 0x01 credential points to a standard Ethereum address.

As mentioned, the Capella upgrade makes it possible for ETH that is “locked” on Ethereum’s CL (i.e. validator balances) to be withdrawn, and credited to an Ethereum address on the EL. For this to happen, the withdrawn validator must have a corresponding Ethereum execution address where its withdrawn balance is sent. In short, the 0x01-type withdrawal credential provides this corresponding execution address, whereas the 0x00-type does not.

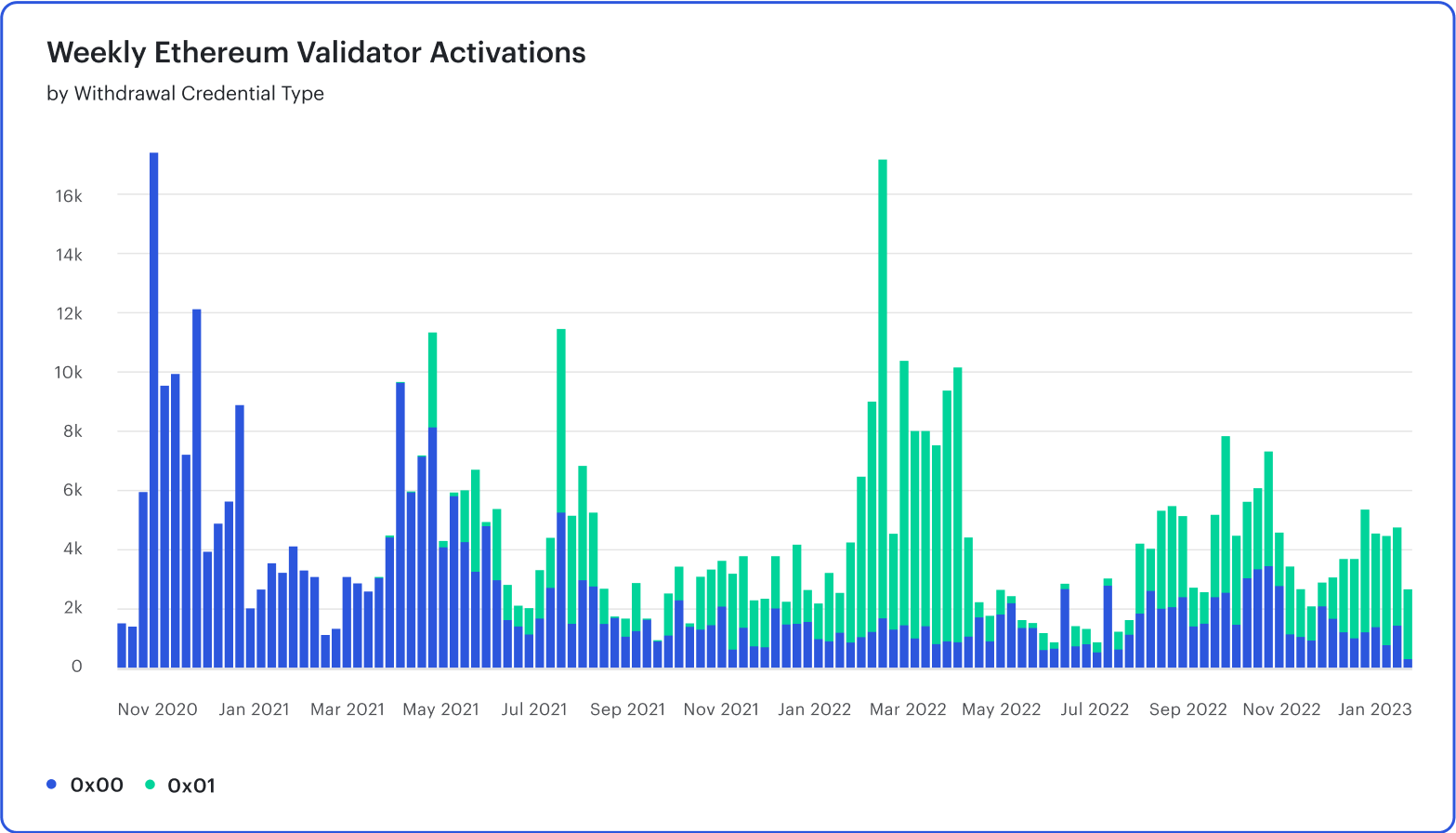

As of February 20, 2023, about 58% of active Ethereum validators had 0x00-type withdrawal credentials. When the Beacon chain launched in late 2020, 0x00 credentials were the only option available, and the newer, 0x01 credentials were not introduced until March, 2021. Hence, all validators activated prior to this date had 0x00 credentials.

As seen in Figure 2, about 20% of newly activated validators still set their withdrawal credentials to the older, 0x00-type. This may be due to solo stakers or institutions using outdated guides to activate validators, or it might be an intentional decision made by stakers who wish to avoid any potential tax implications of automatically receiving liquidity from partial withdrawals. Please note that the tax implications of staking are not yet well-defined in many jurisdictions and this is not tax advice. Tax rules vary by jurisdiction, and a certified professional in your jurisdiction should be consulted for advice.

Figure 2. Weekly Beacon Chain Deposits by Withdrawal Credential TypeSource: Consensys, Dune Analytics, @DataAlways

For 0x00-credentialed validators, the Capella upgrade includes an operation to update their withdrawal credentials to the 0x01-type. Doing so requires the owner of the 0x00-credentialed validator to use their existing withdrawal credentials (BLS key) to sign and submit a withdrawal credentials change message to Ethereum’s CL via a consensys layer client.

Processing Time

The rate at which 0x00-type withdrawal credentials can be updated to 0x01-type is limited to 16 per block (every 12 seconds), per the Ethereum consensys specification. However, unless there is an immediate need for liquidity, 0x00-credentialed validators should feel no pressure to update by any particular date since they will continue to accrue rewards as they have since the launch of the Beacon chain.

Note that once a validator has updated its withdrawal credential from the 0x00-type to the 0x01-type, it can no longer be changed. This is a one-time-only, unidirectional change from 0x00 to 0x01-type withdrawal credentials.

Partial Withdrawals

Partial withdrawals are the periodic “skimming” of validator balances that exceed 32 ETH. This happens automatically for any validator that: has a 0x01-type withdrawal credential, AND is active, AND has a validator balance that exceeds 32 ETH.

Partial withdrawals benefit stakers by providing recurring access to the CL staking rewards their validator has earned (net of any penalties) without incurring any gas costs, or having to exit their validator. Further, since the effective balance of an Ethereum validator is capped at 32 ETH, any surplus ETH on a validator’s balance is unproductive. Partial withdrawals allow stakers to access this surplus, unproductive ETH and redeploy it to activate new Ethereum validators, or elsewhere. Partial withdrawals should also benefit the Ethereum network by preventing an excessively long exit queue and excessive validator churn, which could destabilize the network.

Processing Time

Active validators with 0x01-type withdrawal credentials can expect their validator balance to be partially withdrawn every 2 to 5 days following the Shanghai/Capella upgrade. This is the expected time required for the automated “sweep” to scan Ethereum’s active validator set and process withdrawals for those that are eligible. A range is given, rather than an exact number, since it is unknown how many 0x00-credentialed validators will update to 0x01 credentials immediately after the upgrade is live.

The lower end of this range (2 days) assumes that none of the 0x00-credentialed validators update to 0x01 credentials, keeping them ineligible for withdrawals. The higher end (5 days) assumes all 0x00-credentialed validators update immediately. The reality is likely to be somewhere in between, but there is no data available to support a concrete estimate.

Full Withdrawals

A full withdrawal is the reclaiming of an “exited” validator’s entire balance. The prerequisite step of exiting the validator requires specific, manual actions. However, the withdrawal process happens automatically for any validator that: has a 0x01-type withdrawal credential, AND is exited.

Some other blockchains secured by PoS have an “un-bonding” period, which is a fixed period that a staker must wait after submitting their withdrawal request before gaining access to their previously staked assets.

In Ethereum, rather than an “un-bonding” period with a fixed duration, the full withdrawal period is given by the sum of two processes, each with variable durations: the validator exit process, and the full withdrawal process.

Processing Time

Executing a full withdrawal is a two-part process. First, the validator must be exited from Ethereum’s consensys layer. Then, the validator is subject to the same, automated withdrawal process that executes partial withdrawals, but with an added delay.

In short, the full withdrawal of a validator is expected to take a minimum of 28 hours. This is the sum of the absolute minimum time required to exit a validator (5 epochs, or 32 minutes) and the absolute minimum time required for a validator to become fully withdrawable (256 epochs, or 27.3 hours). Most full withdrawals, however, will take longer than this.

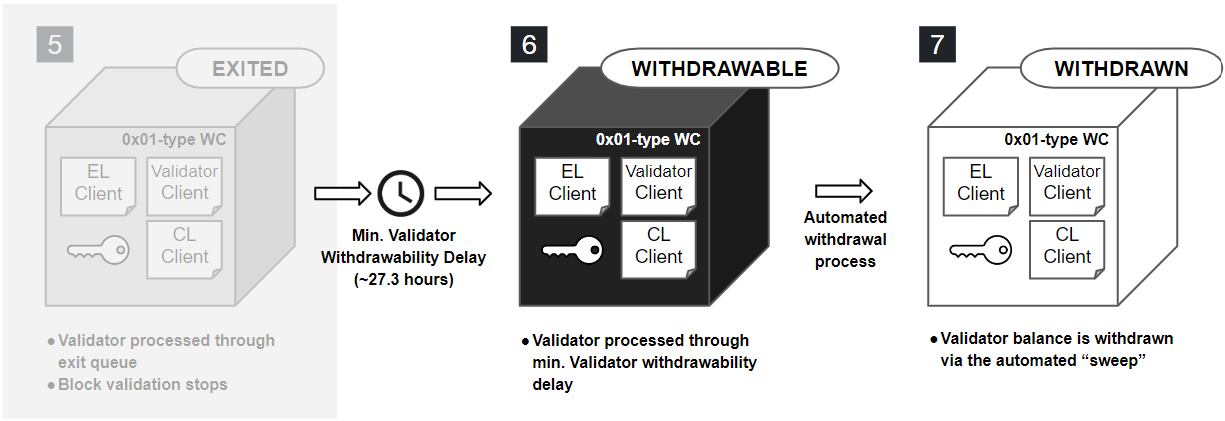

Validator Exit Process

Figure 3. Validator Exit ProcessSource: Consensys

Figure 3 depicts the high-level steps required to exit an active validator. Let’s briefly talk about each step.

An active validator, with 0x01-type withdrawal credentials, proposes and attests to blocks as expected.

The validator’s private key is used to sign a voluntary exit (VE) operation, and the signed VE is submitted to Ethereum’s CL (via a CL client).

A maximum of 16 VEs are processed each slot (every 12 seconds).

Once the VE operation is processed and after a minimum five-epoch (32 minute) delay, the validator’s status is updated from active to exiting. At this point, the exiting validator is assigned an exit epoch (i.e. the epoch in which the validator will be exited), and has officially entered the exit queue. While the validator has now signaled its intent to exit, it still must perform all validator duties (i.e. block proposals and attestations) until it is processed through the exit queue. The length of the exit queue varies depending on the total number of active Ethereum validators and the number of validators already in the queue.

After the validator is processed through the exit queue, its status is updated from exiting to exited, and it stops validating blocks.

Validator Exit Rate Limits

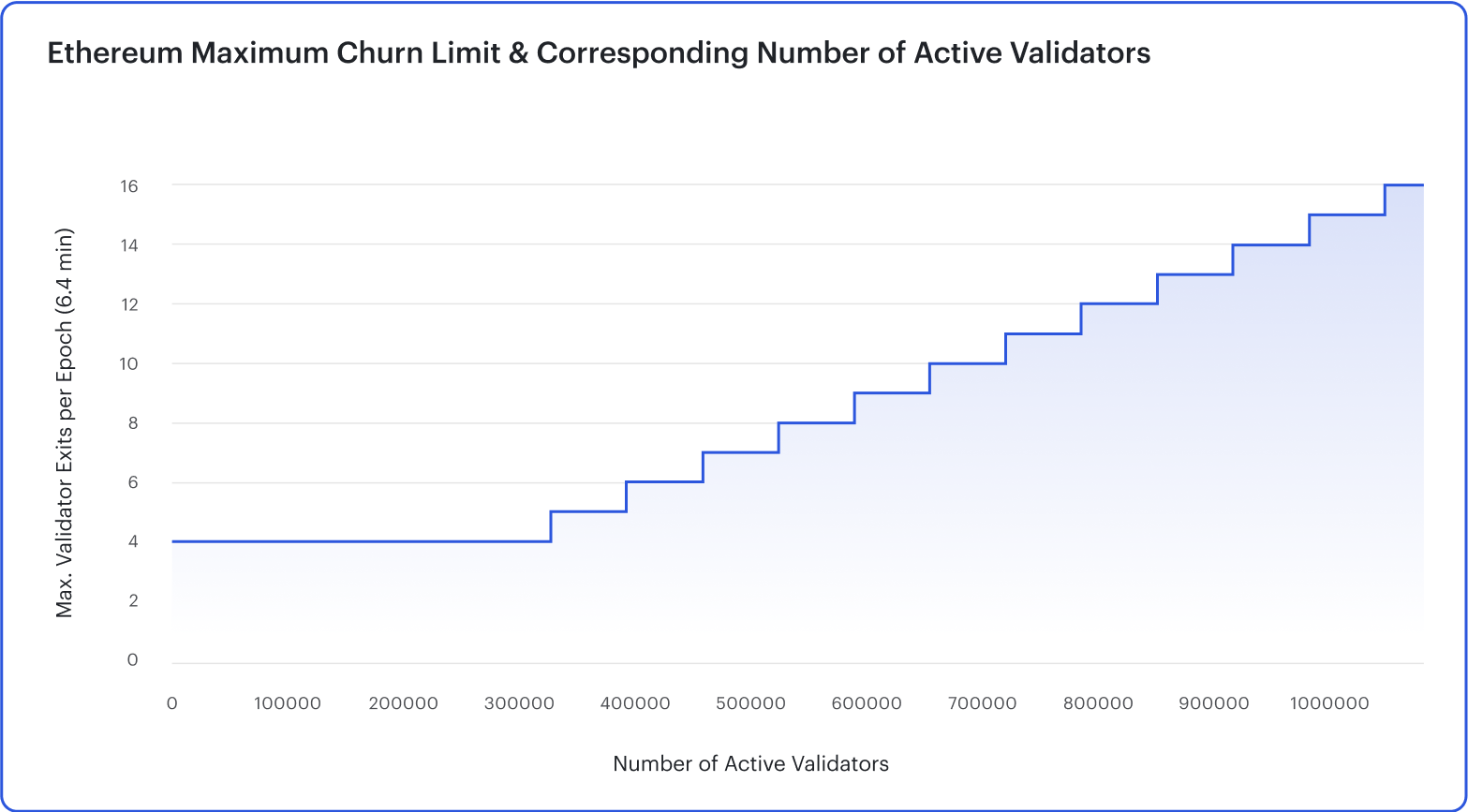

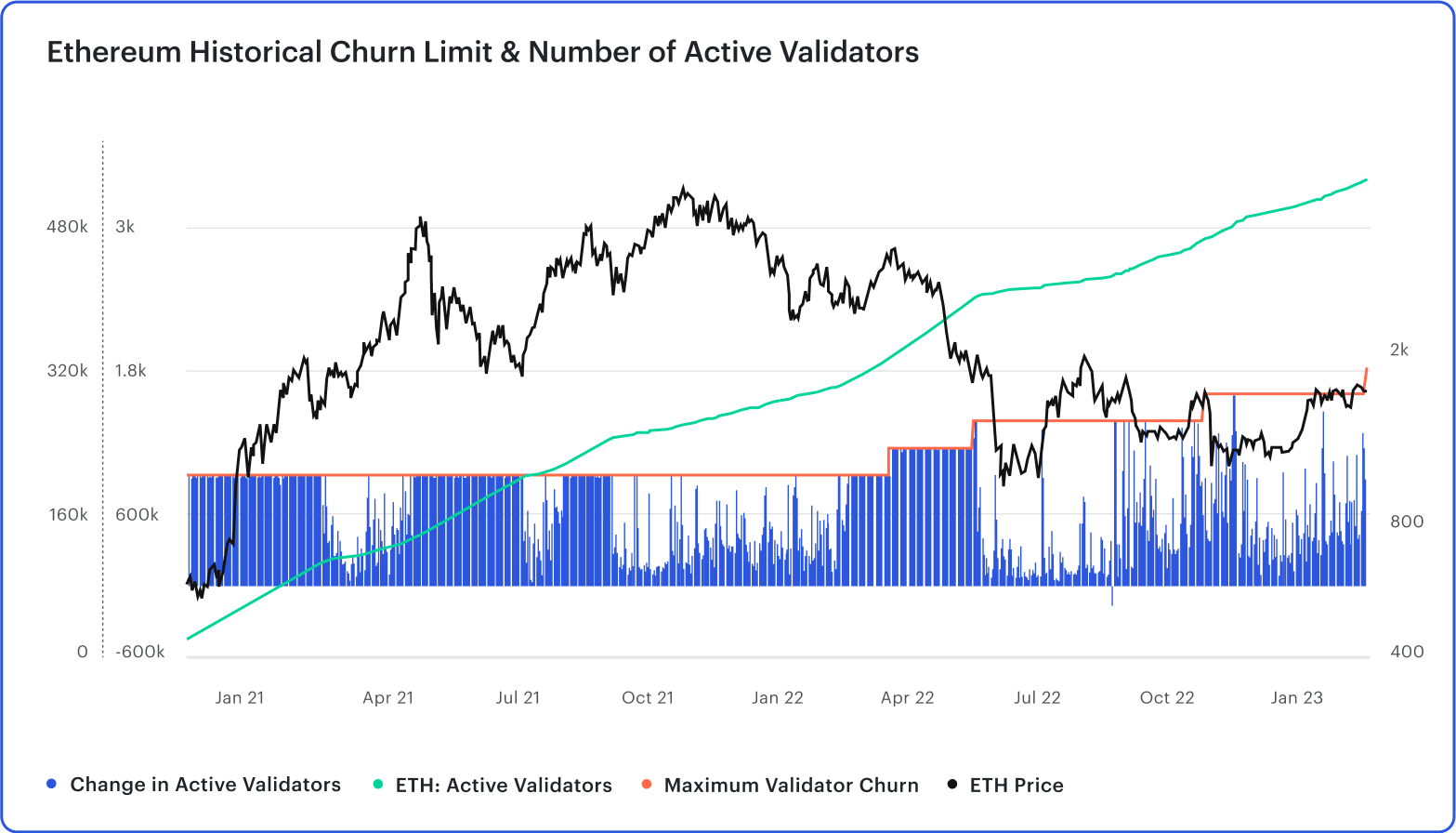

For a number of reasons, it is important that the validator set of a PoS protocol does not change too quickly. Therefore, validator exits are rate limited by the exit queue. The duration of the exit queue is a function of the protocol’s churn limit, and the number of validators to be exited ahead of the validator of interest.

The churn limit is a variable that defines the maximum number of validators that can be exited per epoch (every 6.4 minutes), and is given by the expression:

Churn Limit =max(4, ⌊active_validators/65536⌋)

According to the expression above, the churn limit will be four until there are 327,680 active Ethereum validators, at which point it becomes five. After this point, for every 65,536 newly-activated validators (the churn limit quotient), the churn limit increases by one.

As of February 23, 2023, there are roughly 525,000 active Ethereum validators. From Figures 4 and 5, we can see that the current churn limit is eight, meaning that 1,800 validators can be exited per day (See Figure 4).

Figure 4. Maximum allowable withdrawals per daySource: Consensys

Figure 5. Ethereum Maximum Churn LimitSource: Consensys

Plotting the historical number of active Ethereum validators against the corresponding churn limit yields Figure 6.

Figure 6. Change in Active Ethereum ValidatorsSource: Consensys, Glassnode

Knowing the churn limit and the number of validators to be exited ahead of the validator of interest, the total duration of the exit queue (in days) can be calculated as:

Exit Queue Duration (days) = (((#_of_validators_to_be_exited)/(churn_limit))*6.4 mins)/60/24

Full Withdrawal Process

Figure 7. Full Withdrawal ProcessSource: Consensys

After a validator is exited, there are two steps remaining before it can be fully withdrawn:

The exited validator undergoes an additional 256 epoch (27.3 hour) delay, known as the minimum validator withdrawability delay, before its status is updated from exited to withdrawable.

Finally, the withdrawable validator is subject to the same, automated “sweep” that processes partial withdrawals, and its balance is withdrawn.

Full Withdrawal Rate Limits

As mentioned above, all exited validators must wait 256 epochs (27.3 hours or 1.1 days) until they become withdrawable. Once the validator is withdrawable, the rate at which full withdrawals are processed is limited to 16 withdrawals per slot (every 12 seconds) by the same automated “sweep” process that handles partial withdrawals.

Hence, the expression below gives the maximum amount of time any exited validator should have to wait before it’s balance is fully withdrawn (in days):

Max. Time from Exit to Withdraw (days) ≅ (((withdrawals_eligible_validator_count/16)*12)/60/60/24) + 1.1 days

where “withdrawals_eligible_validator_count” is the number of validators that are eligible for either partial or full withdrawals (since the single, automated “sweep” process handles both types of withdrawals).

Join us as we discuss the tangible effects of the Shanghai/Capella upgrade on the Ethereum ecosystem. Watch the on-demand webinar →

How does the Shanghai/Capella Upgrade Impact the Ethereum Staking Ecosystem?

We have seen above that the Shanghai/Capella fork is poised to “unlock” staked ETH from the consensys layer and make it withdrawable to an Ethereum execution address. Withdrawals will have broad implications for the entire Ethereum staking ecosystem – from the liquid supply of ETH, to the competitiveness of Ethereum staking providers.

Now that we know how the withdrawals process will work, let’s look at how they might impact the liquid supply of ETH.

Liquid ETH Supply

Here, we’ll attempt to understand how the liquid supply of ETH may be impacted by both partial and full withdrawals in the first few days, post-Shanghai/Capella.

Much of this analysis is dependent on staker behavior, and the actions of intermediaries whose exact, post-Shanghai/Capella plans remain unclear. As a result, any conclusions drawn in this section are directional hypotheses, rather than exact predictions.

Pre-Withdrawals

Before we can reason about how partial withdrawals might play out, we need to understand the current, pre-withdrawals state of Ethereum’s active validator set.

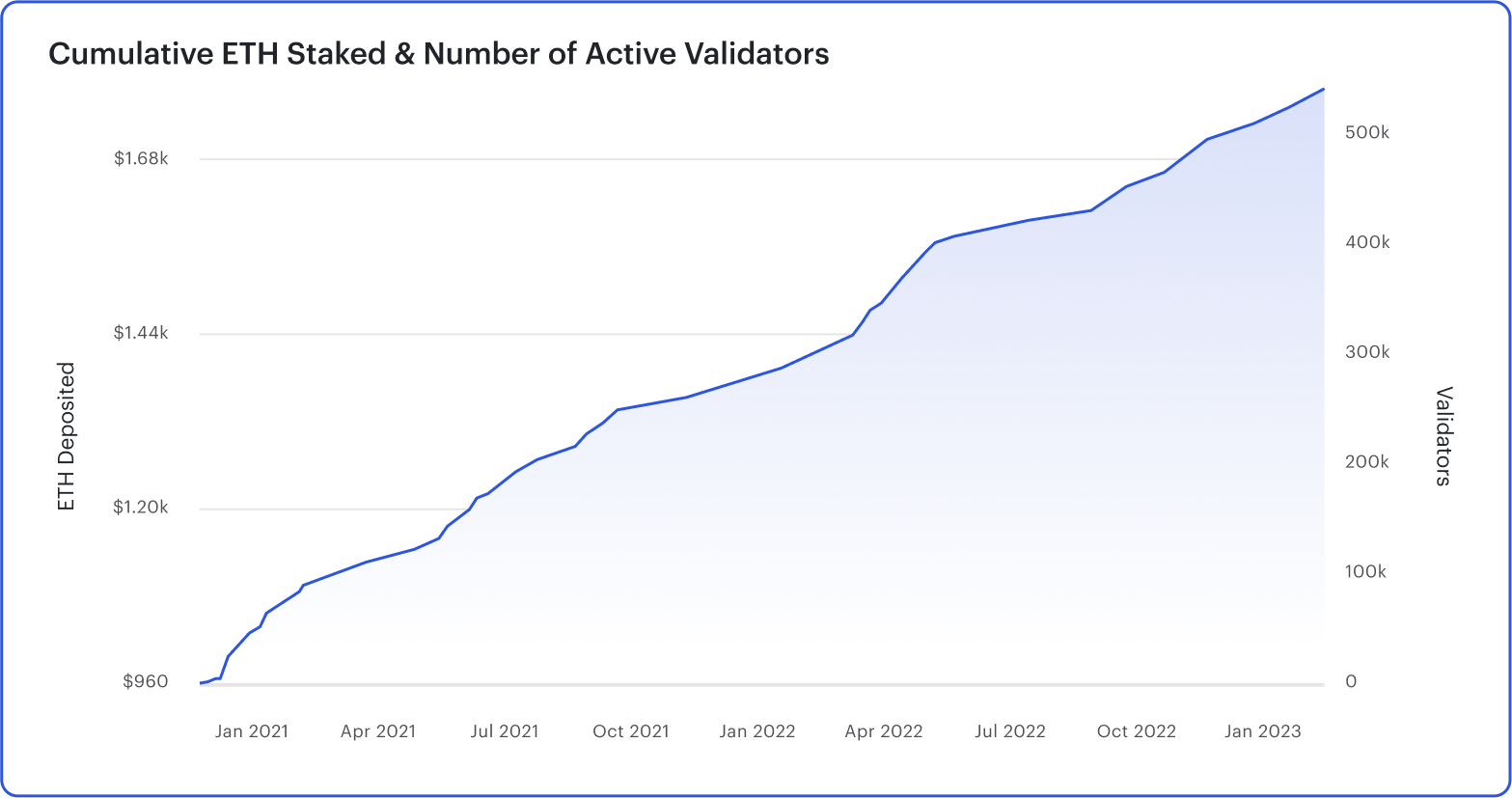

As of February 23, 2023, there are roughly 16.8M ETH staked, which represents 14.6% of the total ETH supply. This staked ETH is deposited to over 525,000 validators and the average validator balance recently surpassed 34 ETH. This suggests that the average Ethereum validator has accrued about 2 ETH in CL rewards to date, and that over 1M ETH could become liquid by way of partial withdrawals, post-Shanghai/Capella.

We can refine our understanding by presenting an analysis conducted by Tripoli of Data Always, in which Ethereum validators are further divided into three subgroups of relevance: 0x00-credentialed, Lido 0x01-credentialed, and non-Lido 0x01-credentialed. Having a more granular understanding of these particular validator subgroups will help qualify our model of partial withdrawals for two primary reasons.

First, we know that only 0x01-credentialed validators will be immediately eligible for partial withdrawals, so the total amount of ETH that partial withdrawals will “unlock” depends on how many 0x00-credentialed validators update to 0x01 credentials, post-Shanghai/Capella.

Second, we know that Lido (like all liquid staking protocols) is likely to re-deposit and stake the ETH that is skimmed from their validators as part of the partial withdrawals process. This is because doing so maximizes the rewards rate of Lido’s liquid staking token, stETH. Knowing this, we can discount the amount of ETH that will be made liquid from partial withdrawals of Lido validators in our model, since it is likely to be immediately re-staked.

Examining the withdrawal credentials of Ethereum’s active validator set through the lens of these three subgroups reveals that 58% have 0x00-type withdrawal credentials. Of the remaining 42%, with 0x01-type withdrawal credentials, about 61% (or 25% of all Ethereum validators) are operated by the Lido validator set.

Figure 8. Ethereum Validator Withdrawal CredentialsSource: Consensys, Dune Analytics, @DataAlways

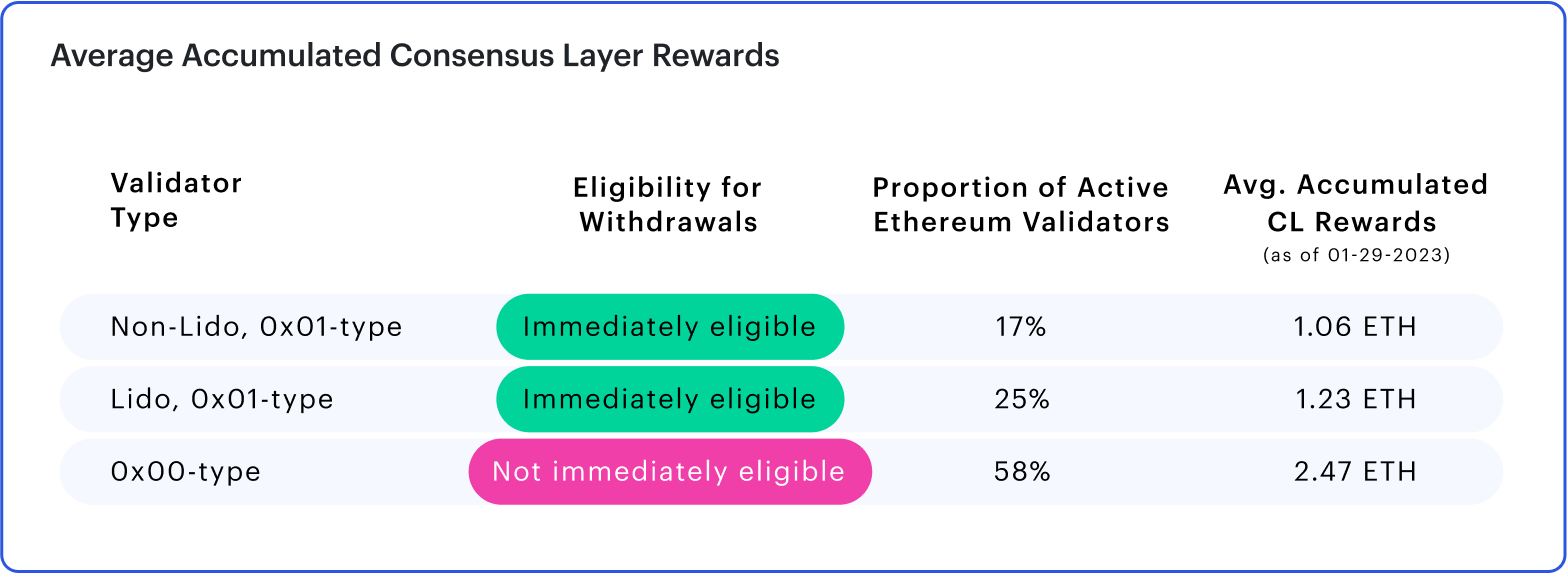

Dividing each subgroup’s total accumulated rewards by the number of validators in each group, gives the average accumulated CL rewards for a typical validator in each subgroup (data as of January 29, 2023 is shown in Figure 9).

Figure 9. Average Accumulated Consensys Layer RewardsSource: Consensys, Data Always

Post-Withdrawals

Partial Withdrawals

Knowing the relative proportion and average accumulated CL rewards of our three validator subgroups, we can begin to reason about how partial withdrawals might play out. Let us consider the first block added to the Ethereum blockchain, immediately following the Shanghai/Capella upgrade.

Since no 0x00-credentialed validators will have updated to 0x01-credentials at this time, the first block will include 16 partial withdrawals exclusively of validators that currently have 0x01 credentials set. Of these 16 validators, we can assume that 61%, 9-10 of them, are operated by Lido, and that the remaining 6-7 are non-Lido 0x01-credentialed validators. If the above holds true, then the first block post-Shanghai/Capella would “unlock” roughly 18.6 ETH (about 11.7 ETH from the Lido 0x01-credentialed validators and about 6.9 ETH from the non-Lido 0x01-credentialed validators).

At the same time that the first block’s worth of partial withdrawals are processed, the first 16 0x00-credentialed validators who’ve submitted a withdrawal credentials change message will have their credentials updated to the 0x01-type, making them eligible to be partially withdrawn. Each block, the composition of validators being partially withdrawn will change to include more previously 0x00-credentialed validators. Since 0x00-credentialed validators are, on average, older and have accrued more CL rewards, this will cause an incremental increase in the total ETH withdrawn per block.

As Tripoli points out, where the profile of ETH withdrawn per block peaks “depends on what percent of 0x00 validators immediately switch their credentials, but in the most extreme case where all 0x00 validators request to change, the profile will peak after 70 hours with partial withdrawals per block of approximately 37.34 ETH – of which 3.01 ETH is from Lido validators”.

The animation below from Data Always shows how much ETH will be unlocked as a result of the first “sweep” through Ethereum’s active validator set, in four different scenarios. The amount of ETH that is unlocked, duration of the sweep, and proportion of each validator subgroup that is included in these partial withdrawals is modeled under the assumption that 25%, 50%, 75% and 100% of 0x00-credentialed validators immediately updated to 0x01 credentials.

Figure 10. Partial Withdrawals if the Shanghai Fork Happened TodaySource: Data Always

Full Withdrawals

As of February 23, 2023, there have been 920 voluntary exits, signaling that these validators intend to fully withdraw. In addition, to settle recent charges laid by the US Securities and Exchange Commission (SEC) against Kraken, the centralized exchange agreed to pay a $30M fine and cease operations of its staking service in the US. Data from Hildobby suggests that Kraken validators account for over 7.3% of all active Ethereum validators. While it’s unclear if all Kraken validators will need to be fully withdrawn, in the most extreme case this would result in 38,000 validators (1.2M ETH) being withdrawn shortly after Shanghai/Capella goes live. Assuming the protocol’s churn limit is eight, processing this number of full withdrawals would take over 20 days.

Beyond this, any estimate of the number of validators that will fully withdraw would be pure speculation.

Given the current pace of new validator activations and the still unknown timeline for the Shanghai/Capella fork, Ethereum’s churn limit is likely to be eight when Shanghai/Capella goes live. This would suggest that up to 1,800 validators (or ~57,600 ETH) could be fully withdrawn per day. As Tripoli points out, if a queue forms to activate new validators and also for full withdrawals, this “double-ended queue will lock the churn limit and effective validator count at a [fixed] value until one side of the queue subsides”.

The plot below (forked and tweaked from Data Always) models how much time it would take to process the full withdrawal of various percents of the active Ethereum validator set. This plot assumes a frozen churn limit of either seven or eight (i.e. that validator exits are matched by new activations). Further limitations of this analysis are that it was conducted with daily step intervals, and it does not consider the validator exit process, the minimum validator withdrawability delay, or partial withdrawals.

Figure 11. Number of days required to exit a given share of Ethereum validators (assuming a locked churn limit, i.e. exits are matched by new deposits)Source: Consensys, Data Always

Competition & Innovation

For most ETH stakers, the Shanghai/Capella upgrade provides the first opportunity to change how, and with whom, they originally decided to stake. Post-withdrawals, the increased portability of stake could set in motion a mass reallocation event that drastically alters the distribution of market share across the Ethereum staking industry.

The risks and opportunities that withdrawals present have been recognized by ETH staking incumbents and new entrants alike, and it’s clear that the industry will become increasingly competitive. This competition is expected to drive rapid technical and business model innovation, particularly amongst liquid staking protocols.

In this section, we provide a snapshot of the innovations and emergent trends being observed across the Ethereum staking ecosystem today, as well as insight into how incumbent staking protocols plan to handle withdrawals.

User Experience

The barriers to entry for ETH staking are being progressively lowered for both retail and institutional stakers. For simplicity’s sake, we will assume that “retail” stakers are likely to stake less than 32 ETH, whereas institutional stakers (or whales) are likely to stake more than32 ETH. In reality, however, there is overlap between these groups.

Retail

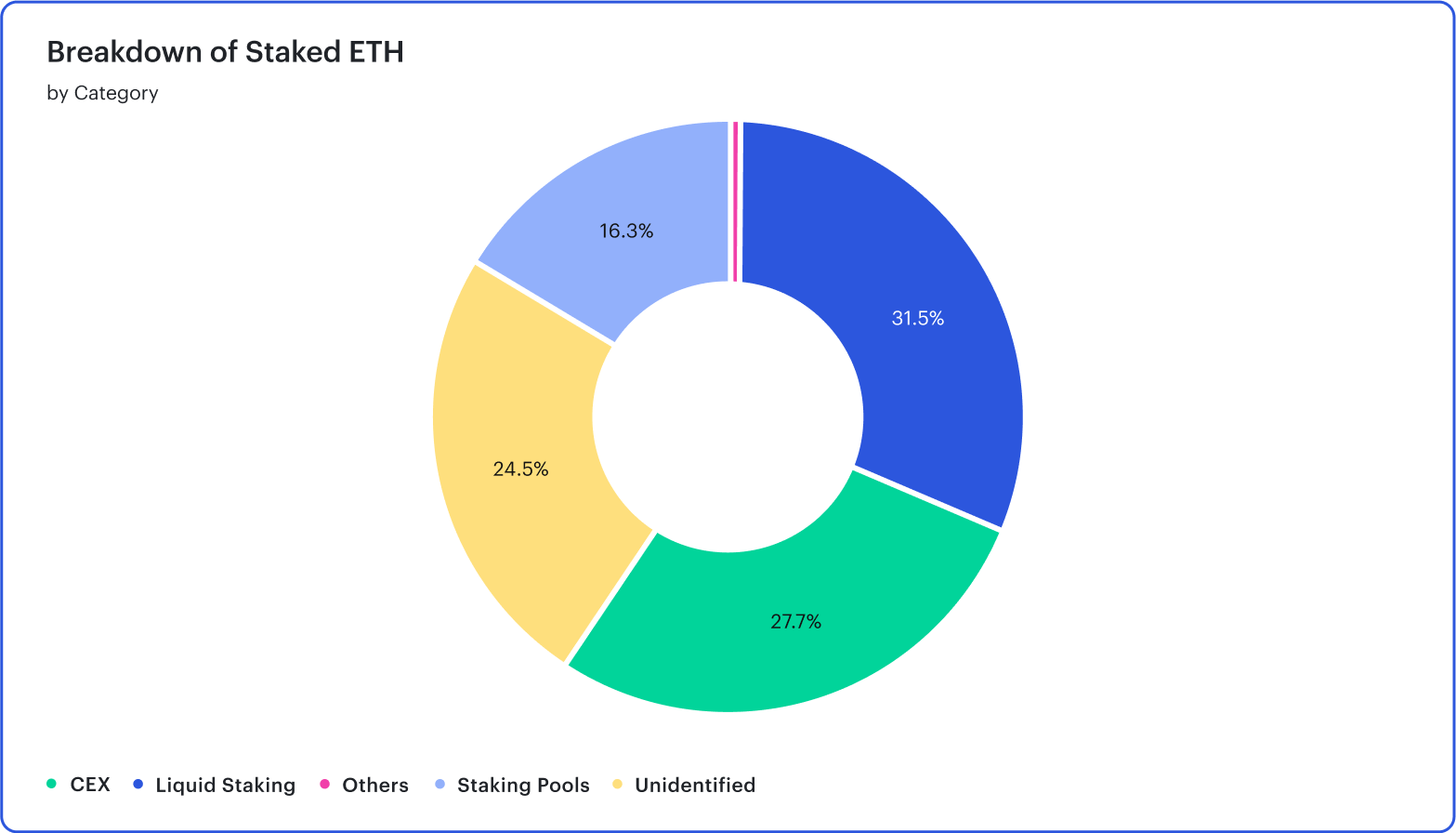

Data from Hildobby shows that, of the about 16.8M ETH staked at the time of writing, over 75% was staked through an intermediary that’s identifiable on-chain. These intermediaries can be a liquid staking protocol (accounting for nearly 32% of all staked ETH), a centralized exchange (accounting for 28%), or a non-liquid staking pool/service provider (accounting for 16% of all staked ETH). The remaining 24% of Ethereum validators are operated by unidentified entities, likely solo stakers.

Figure 12. Breakdown of Staked ETH by CategorySource: Consensys, Dune Analytics, @Hildobby

Liquid staking is often the preferred way to stake, especially amongst retail stakers. This is largely due to the simplified, single-transaction user experience that liquid staking protocols provide, as well as the liquid staking token (LST) that users receive in return for their deposited ETH. This LST provides stakers with a limited form of liquidity on their staking position, and allows them to rehypothecate their staking position elsewhere in DeFi to compound their rewards.

For newcomers to ETH staking, even staking via a liquid staking protocol presents some user experience (UX) hurdles. First, users are required to visit multiple, distinct protocol interfaces and rely on data from unfamiliar sources to compare and, ultimately, select a provider. Once a user has staked, they receive a LST which represents their principle amount staked and accrued rewards. However, these LSTs can be implemented quite differently by different providers, making tracking one’s earned staking rewards a cumbersome and confusing process. Early 2023 saw the launch of two exciting ETH staking products that aim to solve these UX issues.

MetaMask Staking provides users the ability to stake their ETH with Lido or RocketPool from within MetaMask’s portfolio dapp. The familiar MetaMask interface is accompanied by helpful information about Ethereum staking. Beyond connecting users to top liquid staking protocols, MetaMask Staking’s rewards-tracking interface provides users with an estimate of the rewards they have received from their staking position.

In addition, other structured products are emerging that provide users with access to a diversified basket of LSTs. One such product is Index Coop’s diversified staked ETH (dsETH), which is an index composed of Rocket Pool’s rETH, Lido’s stETH, and StakeWise’ sETH2 token.

Institutional

While there are certainly exceptions, those with more than 32 ETH may be more likely to stake with a staking-as-a-service provider, rather than a liquid staking protocol, for the following reasons:

Increased security and reliability of working directly on the validator operator (without an intermediary)

Traceability between staked funds and specific validators

Stronger operational assurances (e.g. SOC2 compliance)

Better control over the exact infrastructural setup of each validator

Lower fees

Better financial and tax reporting

For example, staking providers like Consensys Staking promise increased security and reliability (SOC2 Type II Certified) alongside reduced risks of highly correlated outages. Consensys Staking mitigates these risks with a validator infrastructure that is distributed across multiple cloud providers, regions, Ethereum clients and MEV relayers.

Like retail users, institutions must compare and select between multiple options and face a disjointed user experience across various staking providers.

Other emerging innovations that institutions should keep on their radar are the launch of the Liquid Collective’s institutional-focused liquid staking token, LsETH, and a validator NFT concept introduced by Stakefish.

Learn more about how the Shanghai/Capella upgrade will drive competition and innovation, and what this means for retail and institutional stakers. Watch the on-demand webinar →

Liquid Staking Infrastructure

In anticipation of the risks and opportunities withdrawals present, liquid staking incumbents have been developing upgrades to their core protocol infrastructure. These upgrades are an attempt to improve their offering for users and the broader Ethereum community.

Let us briefly look at the next planned upgrades to the Lido, Rocket Pool, and StakeWise protocols. We will then explore some new entrants to the Ethereum staking space.

Upgrading Incumbents

Lido V2

Lido is by far the most dominant liquid staking protocol on Ethereum today, having captured over 29% of the 16.8M ETH that has been staked to date. Throughout the protocol’s history, Lido has had a single, permissioned validator set.

Currently, this validator set consists of 30 professional validator operators, who are able to activate new Ethereum validators without any capital requirements, or bond, being supplied by the validator themselves. This highly scalable model, in combination with stETH’s extensive DeFi integrations, has led to Lido’s outsized success. However, as the proportion of Lido’s stake approached a third of all staked ETH, it led to centralization concerns from prominent members of the Ethereum community.

Recently, the protocol announced Lido V2 as an important step towards further decentralization. Lido V2 is centered around two major upgrades: withdrawals and the staking router.

Withdrawals

Lido’s exact implementation of withdrawals remains to be confirmed, however the protocol has released a proposal for community review and feedback.

In short, Lido proposes a two-step, “request-claim process” for stETH holders. Users submit withdrawal requests to the protocol and are issued an NFT that represents their position in a Lido-specific queue. Interestingly, these NFT queue positions will be tradable, allowing users who require immediate liquidity to “jump the queue”, likely by paying a premium. The protocol then calculates the stETH:ETH redemption rate for each request, reserves the amount of ETH necessary to fulfill the request, and burns the corresponding amount of stETH.

Liquidity to facilitate withdrawals may come from EL rewards, partial or full withdrawals of Lido validators, new user deposits, or a combination of these sources. Once the reserved, liquid ETH is available, the user can claim this ETH.

Lido’s in-protocol withdrawal queue will be processed in one of two modes: “turbo” or “bunker” mode. From the user’s perspective, the key difference between these modes is the period of time they must wait between submitting a withdrawal request, and claiming their ETH. The protocol enters “bunker” mode in the event that a significant number of Lido validators (upward of 600) are slashed. “Bunker” mode is designed to halt withdrawals until all slashing penalties are accounted for to ensure the stETH:ETH redemption calculation can be performed accurately. In “bunker” mode, withdrawals could be delayed for upwards of 36 days.

Staking Router

Fundamentally, Lido V2 enables the protocol to move away from having a single, permissioned validator set, in favor of onboarding multiple distinct validator subsets, called modules. The staking router is the core piece of infrastructure that will orchestrate how new user deposits to Lido are distributed to different modules. Initially, the Lido DAO will set a target percentage of all active Lido validators that each module can support.

No timeline has been provided for when Lido V2 will be live on Ethereum mainnet, however it’s expected to roll out in phases. For example, withdrawal functionality is likely to be prioritized over the launch of the staking router in its final form.

Rocket Pool’s Atlas Upgrade

In November 2021, Rocket Pool introduced minipools to the Ethereum staking ecosystem. Minipools reduced the capital requirements of operating an Ethereum validator by 45%. Operating a Rocket Pool minipool requires just 17.6 ETH (16 ETH bond, plus 1.6 ETH worth of RPL collateral), as compared to the usual requirement of 32 ETH.

What differentiates Rocket Pool as a liquid staking provider is the fact that its validator set is permissionless, meaning that anyone who meets the minimum bond requirement can operate a minipool. This bond requirement is essential to the protocol’s health and the competitiveness of the rETH token, as it aligns the incentives of minipool operators and rETH token holders. If a minipool is slashed, the operator’s 16 ETH bond and 1.6 ETH worth of RPL collateral will incur losses ahead of any rETH token holder. This design incentivizes minipool operators to perform to the best of their ability, and ensures rETH token holders staked funds are insured by 110% of their value.

Rocket Pool’s high bond requirement has led to an inability to scale as quickly as its competitors with permissioned validator sets. Throughout its history, the protocol has seen multiple instances when the rETH deposit pool reached its maximum capacity (currently 5,000 ETH). This forced prospective stakers to wait until new minipools were activated by the permissionless validator set, purchase rETH on secondary markets, or stake with one of Rocket Pool’s competitors.

In the coming months, Rocket Pool plans to launch its much-anticipated Atlas upgrade. Among other things, this upgrade is designed to handle withdrawals, and improve the protocol’s scalability.

Withdrawals

Liquidity to support withdrawals will be sourced from the protocol’s deposit pool, and a portion of the ETH that will be made liquid via partial withdrawals of Rocket Pool validators.

Since minipools are operated permissionlessly, the protocol has no ability to force an operator to exit and withdraw their validator balance. In the event that rETH redemptions exhaust the liquidity available in the deposit pool and from partial withdrawals, the protocol will rely on open market arbitrage opportunities to incentivize minipool operators to exit and fully withdraw their validators.

Presumably, if rETH cannot be redeemed for ETH via protocol-supplied liquidity, users will turn to secondary markets where excessive rETH supply will cause it to trade at a discount. Once this discount becomes attractive enough, rational minipool operators should be incentivized to purchase 16 rETH at a discounted rate, burn it via Rocket Pool’s smart contracts, and exit/withdraw their minipool. Doing so would allow them to pocket the difference between the smart contract’s rETH:ETH exchange rate, and the discounted exchange rate rETH is trading at on secondary markets.

Scalability

To more effectively scale, Rocket Pool’s Atlas upgrade will reduce the minimum bond requirement of minipool operators from 16 ETH and 1.6 ETH worth of RPL, to 8 ETH and 2.4 ETH worth of RPL. This will reduce the capital requirements of operating an Ethereum validator by 67.5%, from 32 ETH to just 10.4 ETH. It will also enable current minipool operators to divide their 16 ETH minipools into two 8 ETH minipools, effectively tripling the rETH minting capacity of each minpool operator.

Further, the Atlas upgrade will also present an opportunity for solo-stakers with 0x00-credentialed validators to join the protocol by updating their validator’s credentials to Rocket Pool’s smart contracts. By doing so, solo stakers will be able to split their 32 ETH validator into 4, 8 ETH minipools. This will allow them to support the minting of 96 rETH, drastically increasing both the protocol’s capacity to meet new rETH demand, and the solo staker’s earning potential

In anticipation of the protocol’s massively increased capacity to support rETH demand, the rETH deposit pool will be increased from 5,000 ETH to 18,000 ETH. This will also help deepen the protocol-supplied liquidity that will enable rETH redemptions.

No timeline has been provided for the launch of the Atlas upgrade, but it’s expected to be launched roughly around the time of the Shanghai/Capella upgrade.

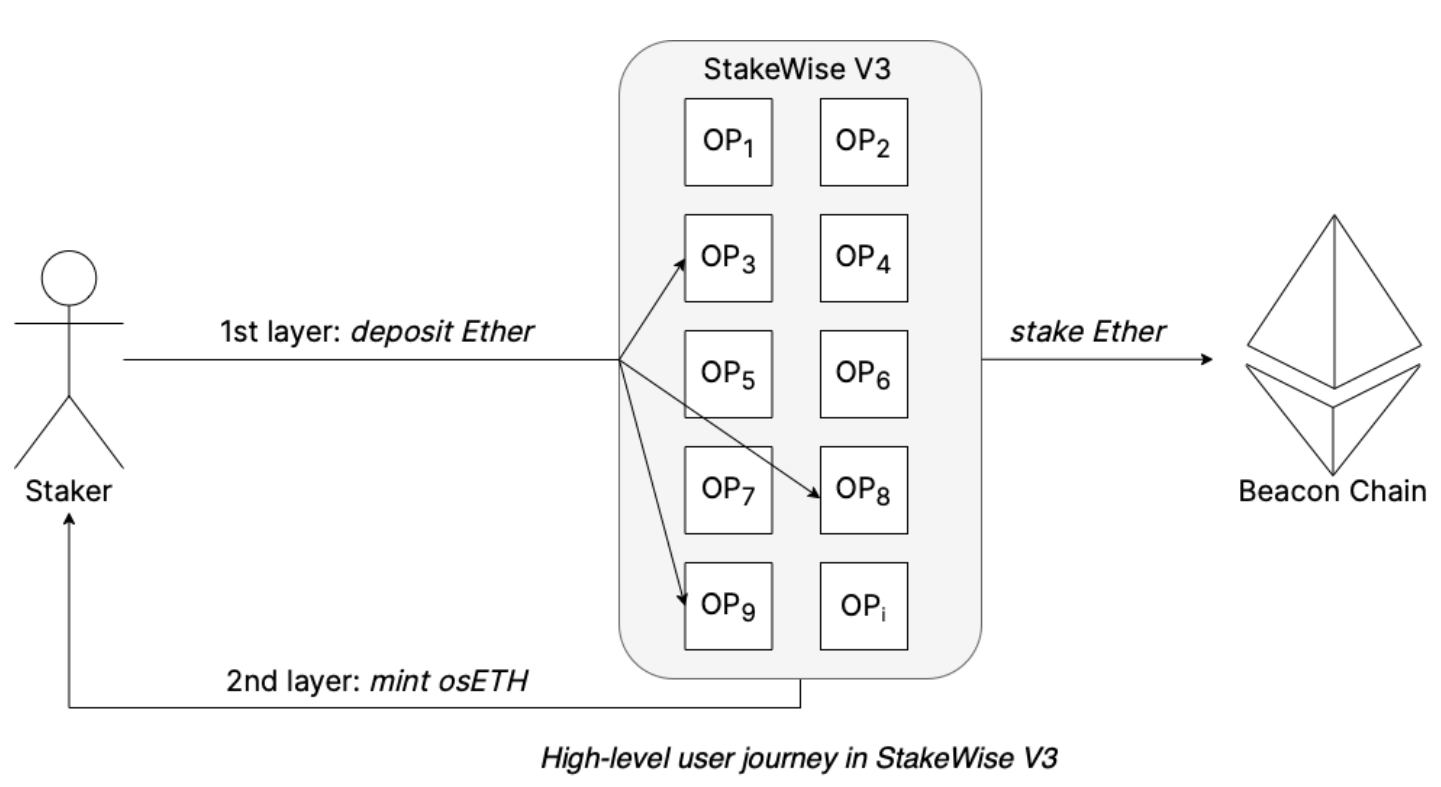

StakeWise V3

StakeWise is currently the fifth most popular liquid staking protocol on Ethereum. Historically, StakeWise’ primary offering was StakeWise Pool which, like Lido, featured a permissioned validator set and a 10% commission on earned staking rewards shared equally between the StakeWise DAO and the validator set.

However, in response to concerns of increasing centralization risk within the ecosystem, StakeWise Labs proposed a major protocol upgrade in September 2022. This upgrade is called StakeWise V3, and can be thought about in two parts, or layers.

Figure 13. User Journey in StakeWise V3Source: StakeWise

Vaults & VLT Tokens

The first layer involves a marketplace of “vaults” or deposit pools that provide stakers with full control over where they stake their ETH. Each vault is essentially its own pool, and can be set up permissionlessly by anyone from a solo staker, to a professional validator operator. The creator of a vault can customize a number of the pool’s parameters, including who can deposit to the pool, who can participate as a validator operator, the vault’s fee structure, etc. Users can browse the available vaults through StakeWise’ UI, and stake with whichever one(s) meet their needs. To help users make informed decisions, each vault is assessed against a transparent set of criteria and assigned a score within the StakeWise UI.

When a staker deposits to a specific vault, they are issued a proportional amount of VLT tokens in return. VLT tokens are repricing ERC-20 tokens, meaning their value relative to ETH increases as the vault earns staking rewards. VLT tokens are unique to the vault that issues them and accrue rewards based on the performance of that specific vault’s validator set. This means that only VLT tokens issued from the same vault are fungible.

Overcollateralized Staked ETH (osETH)

The second layer of StakeWise V3 is where the protocol’s liquid staking token, osETH, is introduced. VLT token holders can mint osETH, or overcollateralized staked ETH, by depositing their VLT tokens into a “collateralization contract”. Notably, the value of osETH tokens that can be minted will always be less than the value of the deposited VLT tokens. Like a collateralized debt position (CDP) in the MakerDAO system, each osETH minter will have a unique loan-to-value metric which reflects the utilization of their VLT collateral in minting osETH. The maximum allowable loan-to-value metric is expected to be about 90%, reflecting the amount of VLT tokens a staker can make liquid, whilst still earning staking rewards on 100% of their ETH staked into a specific vault.

Like VLT tokens, osETH is a repricing ERC-20 token. However, unlike VLT tokens, osETH tokens are not tied to a specific vault’s validators. Rather, osETH tokens accrue rewards at the average rate of all validators across all vaults in the StakeWise v3 system. While this removes traceability between a user’s deposit and a specific validator set, it means that all osETH tokens are fungible and widely usable throughout DeFi.

StakeWise V3 is not yet live on Ethereum mainnet.

New Entrants

A number of additional liquid staking protocols, each with unique and interesting offerings, have launched or plan to launch on Ethereum mainnet in the coming weeks and months. Let us explore some interesting protocols to watch.

Frax

Frax Finance, issuer of the well-known FRAX stablecoin, is now the fourth most popular liquid staking offering on Ethereum. According to data from DefiLlama, over the past 30 days, Frax has seen a 40% increase in total value locked. The protocol’s meteoric rise in the Ethereum staking space is due to the outsized rewards holders of sfrxETH (staked Frax ETH) have earned relative to other LSTs over the past few months. As of February 23, 2023, sfrxETH’s average rewards rate over the past 30 days was ~7.4%, more than two full percentage points higher than the market leader, Lido’s stETH.

This is how sfrxETH provides such a high rewards rate:

Before a user can mint sfrxETH, they must first deposit ETH to the protocol and mint frxETH (Frax ETH).

All ETH that is swapped for frxETH is staked by the Frax protocol. However, frxETH does not accrue staking rewards like Lido’s stETH or Rocket Pool’s rETH. Rather, it is pegged by the protocol at a 1:1 redemption rate with ETH.

From here, frxETH holders have a choice between two options:

Holders of the frxETH token can begin accruing staking rewards by depositing their frxETH into an ERC-4626 vault, and minting sfrxETH. Like other LSTs, sfrxETH accrues staking rewards.

Alternatively, frxETH holders can deposit their frxETH into the frxETH/ETH liquidity pool on Curve to earn rewards paid out in CRV, CVX, and FXS tokens.

Since frxETH holders have two, competing options where they can earn significant rewards, the number of sfrxETH holders is likely to be less than the number of frxETH minters. Hence, the staking rewards earned by the protocol are split between fewer users, and sfrxETH holders are likely to accrue rewards at a higher rate than other LSTs.

Currently, it is assumed that core members of the Frax team operate all of the validators that support the Frax staking offering, however no documentation exists on this topic.

Geode Finance

Geode Finance, like the vault-layer of StakeWise V3, intends to provide permissionless infrastructure that allows anyone to create a public or private staking pool with customizable parameters. Public pools accept deposits permissionlessly, whereas private pools accept deposits only from approved entities. Each pool is meant to be governed in a self-sovereign manner, and will issue its own LST (called a G-derivative in the Geode system).

G-derivatives can be implemented as an ERC-20 (either rebasing or repricing), or an ERC-721 (NFT).

Stader Labs

Stader Labs plans to launch a multi-pool liquid staking protocol featuring permissionless, permissioned, and DVT-enabled pools (once the technology matures). Stakers are issued ETHx, the protocol’s LST, which is a repricing ERC-20 token. Anyone who provides a 4 ETH minimum bond can operate a validator for the permissionless pool. The permissioned pool’s validator set, however, will be community-curated and require no bond from operators. Stader proposes a 10% fee on staking rewards earned by the protocol’s validators, and emphasizes their ability to build a DeFi ecosystem around their LST as a key differentiator.

Diva Labs

Diva Labs plans to offer a liquid staking protocol with a single deposit pool where stakers can deposit their ETH in exchange for divETH, a rebasing ERC-20 token. However, Diva’s key differentiator is that its validator set will be composed exclusively of validators running DVT software. This should make each validator more resilient, and promote validator diversity and decentralization. However, by exclusively offering a DVT-based solution, Diva’s mainnet launch may be delayed as this technology is still maturing. Diva anticipates that validator operators will be required to bond a minimum of 1 ETH to participate.

Swell Network

Finally, Swell Network is planning a guarded mainnet launch of the protocol’s new architecture in April 2023. The first iteration of Swell’s new architecture will feature a permissioned validator set, composed of professional node operators. Stakers will be issued swETH, a repricing ERC-20 token, and will be charged a 10% fee on earned staking rewards.

Emerging Technology

Here, we look at two middleware technologies in the Ethereum validator stack that have the potential to improve validator resilience and the decentralization of the network in the coming months and years. Namely, these are distributed validator technology (DVT), and EigenLayer’s re-staking primitive.

Distributed Validator Technology

Distributed validator technology (DVT) is a technique for distributing the duties expected of a single validator across a set of distributed validators. The goal of distributing validator execution across multiple nodes is to improve the resilience of the validator (safety, liveness, or both), compared to running a validator on a single machine. So long as at least ⅔ of the validators in a DVT setup are functional, the others can go offline, perform poorly, or even be hacked without as severe, or any, penalties being incurred.

Work is ongoing by a dedicated group of researchers at Consensys to formalize DVT. At the same time, Obol Labs and SSV Network are implementing separate versions of the DVT protocol and are both currently live with public testnets.

Re-staking

In recent months, the concept of re-staking has gained immense attention. In particular, EigenLayer has proposed extending the cryptoeconomic security provided by Ethereum’s network of validators to services beyond the Ethereum protocol itself. Functionally, the rehypothecation of consensys layer ETH would require Ethereum validators to set their withdrawal credentials to the EigenLayer smart contract. From here, a staker could opt-in to provide validation services and cryptoeconomic security for an application built on EigenLayer. Opting in would involve accepting additional slashing criteria defined by the application, in exchange for increased staking rewards.

Recently, EigenLayer founder Sreeram Kannan pointed out that there are two types of security that a sufficiently decentralized network of validators can provide: economic security, and decentralized security.

Economic security is provided by the existence of enforceable slashing conditions on staked assets. Briefly, consider two cryptoeconomic systems. One is secured by a single entity who has staked $10B USD of assets which could be slashed for bad behavior. The other is secured by 10,000 distinct entities who have each staked $1M USD of slashable assets. In both cases, the economic security provided by the staker(s) is the same, equivalent to $10B USD.

Decentralized security, however, comes not from the value of the staked, slashable assets, but rather, from the fact that the entities who’ve staked are sufficiently distributed and unlikely to collude. Through EigenLayer’s re-staking primitive, this property of decentralized security can, for the first time, be metered and rewarded by services who require it. In this way, decentralized staking pools and solo-stakers alike could have opportunities to earn rewards from applications built on EigenLayer that their more centralized counterparts won’t be able to participate in.

For all its benefits, there are also some risks associated with re-staking. Validators who opt-in to provide security for protocols beyond Ethereum put their staked ETH at increased risk of unintentionally being slashed. The risk this poses to Ethereum could be significant, especially if a sufficiently large proportion of Ethereum’s active validator set opts-in to provide validation for a single protocol. More comprehensive risk analyses on this topic are likely underway by the EigenLayer team and others.

In addition, EigenLayer’s proposal of establishing a “committee”, with the power to veto slashing decisions made by EigenLayer services, has been met with concern from some members of the Ethereum community. The argument in favor of the committee is that it prevents a mass-slashing event, or series of events, from being carried out if these slashings could put Ethereum at risk. The argument against this is that the “committee” could present a centralization risk that diminishes the substantial efforts that have been made to date to decentralize every layer of the Ethereum tech stack. It remains to be seen who might comprise the proposed committee, and how these individuals will be selected, and either on-boarded or off-boarded, to serve on the committee.

Join us for a discussion on how the Shanghai/Capella upgrade furthers ecosystem development and what that means for users. Watch the on-demand webinar →

Impact of Shanghai/Capella Upgrade on DeFi

Ethereum’s move to Proof of Stake reduced new ETH issuance by 88%. This staggering reduction in ETH issuance, in combination with the EIP-1559 burn rate, has led to the most deflationary moment in Ethereum’s history. (See Figure 14)

Figure 14. Ethereum’s Net Supply After the MergeSource: Consensys, Glassnode

It also gave rise to a new wave of liquid staking protocols that provide a simple way for users who hold less than 32 ETH to combine, or “pool”, their deposits with others. Together, users can fund a new validator once the pool’s value exceeds 32 ETH, and earn staking rewards in proportion to their deposit. After depositing to the pool, the user is issued a liquid staking token (LST), which is an ERC-20 token that represents the user’s principal amount staked, and accrued rewards over time.

Beyond providing easier exit liquidity from staking positions, LSTs can be used across DeFi as collateral assets, so holders can compound their earned staking rewards. These valuable characteristics of LSTs have led to their continued popularity in recent months.

The adoption of LSTs on Ethereum has already resulted in strong growth in staked ETH on the network. Staked ETH increased by 80% to 15.9M over the course of 2022. At the time of writing, ETH was distributed across over 525,000 validators. (See Figure 15)

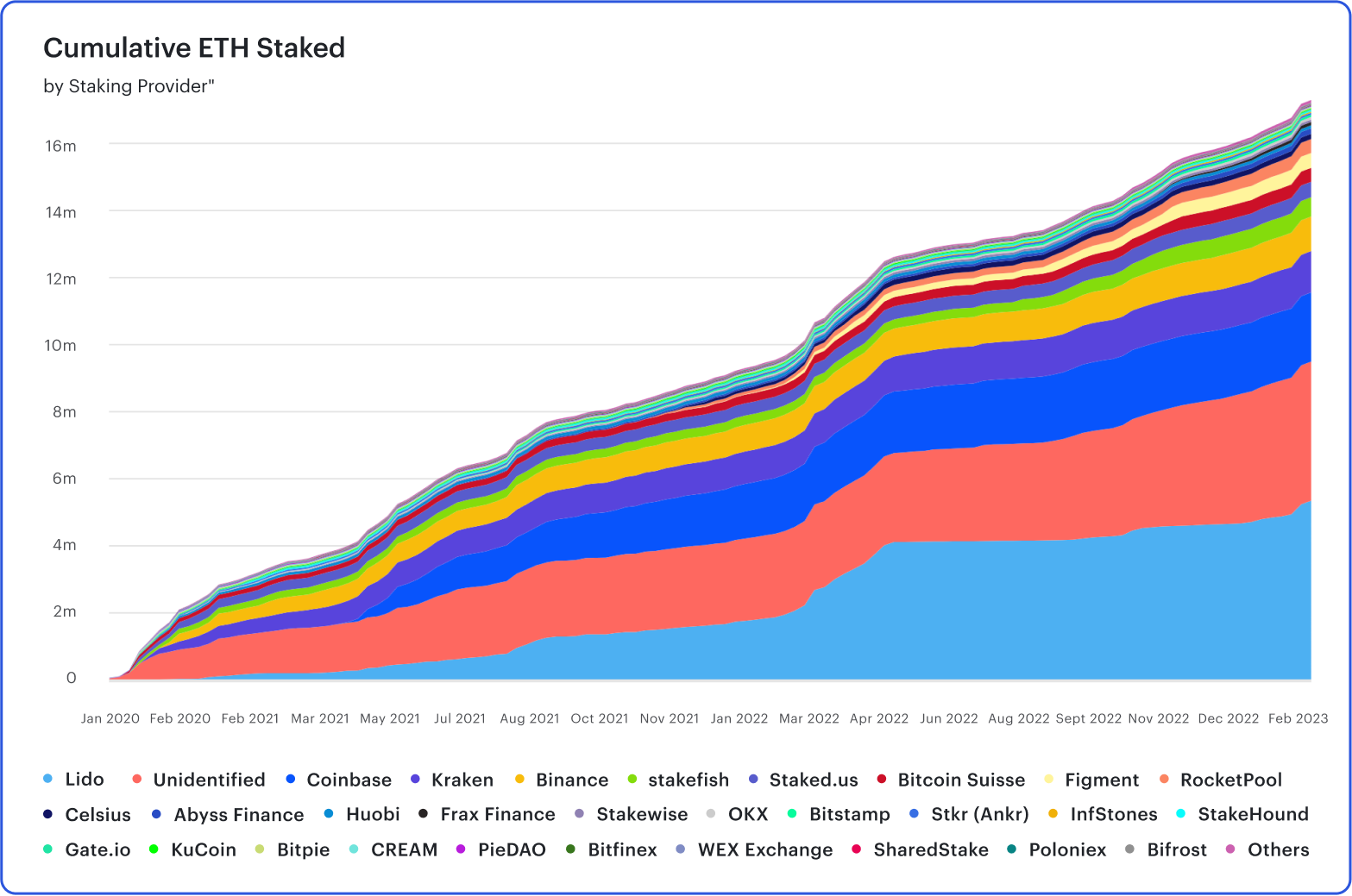

Liquid staking providers are the largest contributors to staked ETH, having captured nearly 32% of the entire ETH staking market, up from 20% at the start of 2022. (See Figure 16) The largest liquid staking provider is Lido, which alone comprises over 29% of all ETH staked on Ethereum.

Figure 15. Amount of ETH Staked Across All ValidatorsSource: Consensys, Dune Analytics, @Hildobby

Figure 16. Cumulative ETH Staked by Staking ProviderSource: Consensys, Dune Analytics, @Hildobby

As mentioned above, up until the Shanghai/Capella upgrade, all staked ETH and accumulated consensys layer rewards have remained locked. This meant that despite liquid staking tokens representing a claim on the underlying ETH, there was no mechanism to redeem it. The Shanghai/Capella upgrade is, therefore, expected to reduce the liquidity risk associated with staking ETH, which in turn has several implications on the DeFi ecosystem.

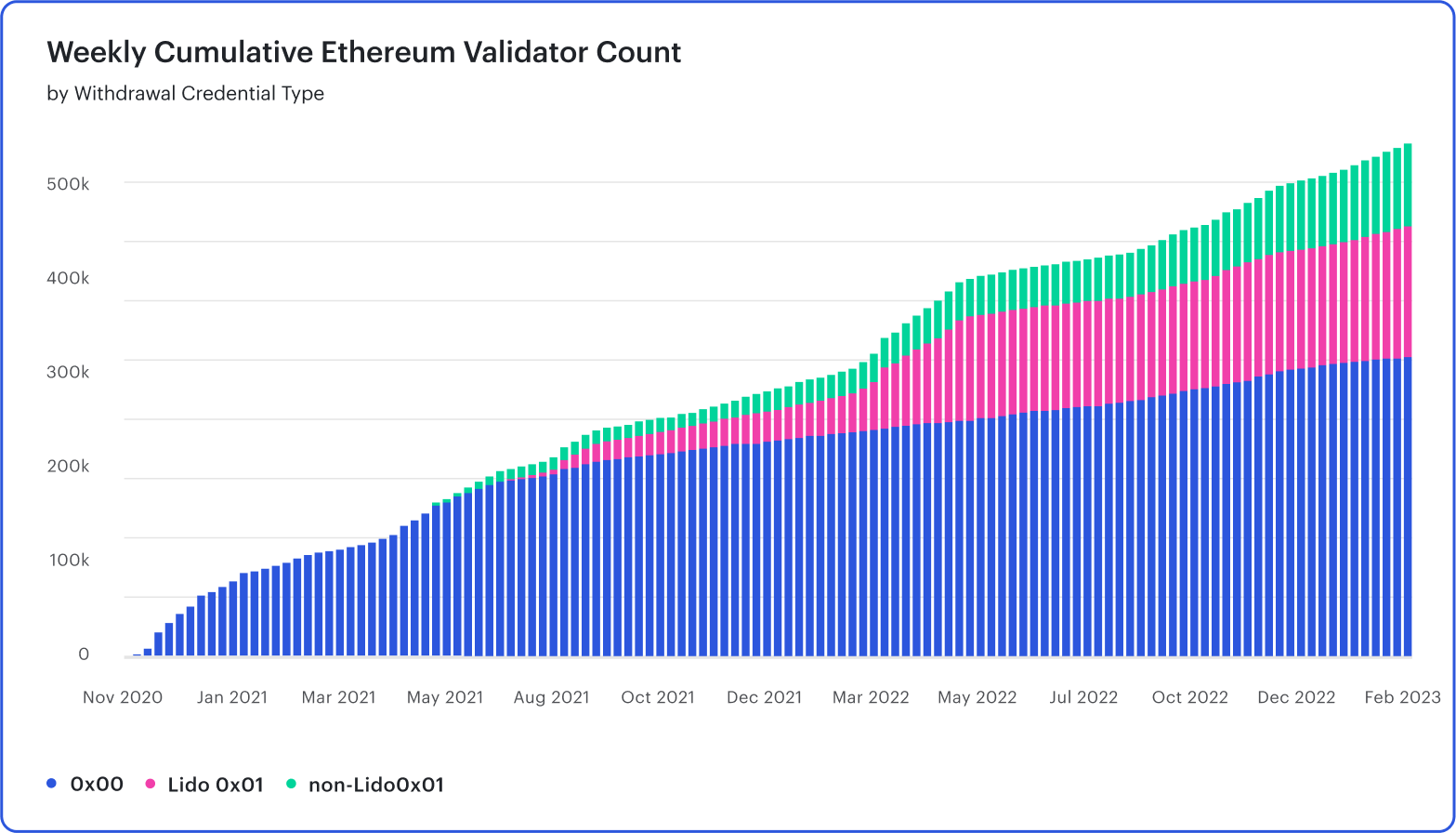

The first is the potential for a large number of ETH withdrawals by long-term validators who will be eager to redeem their accumulated rewards. However, validator distribution and the mechanism for withdrawal suggest sell pressure will likely be more limited. Most long-term validators are identifiable on-chain by their 0x00 credentials, which make up 58% of all validators. (See Figure 17). According to DataAlways, long-term validators have an average of 2.47 ETH rewards for a combined ~770 ETH (about $1.3B). That represents around 0.6% of ETH market cap, excluding initial stake, which would likely have a notable market impact if sold instantaneously.

However, only 16 validators can withdraw per block and only 0x01 credentialed validators (not long term holders) are eligible for withdrawals. This means it is likely that the flow of long-term holders exiting positions will be gradual. Additionally, CL rewards redeemed by liquid staking providers, such as Lido, are more likely to be used to activate new validators as demand for staking increases.

Figure 17. Validator Count by Credential TypeSource: Consensys, Dune Analytics, @DataAlways

Another likely development is a growth in usage of liquid staking providers driven by the reduced liquidity risk of staking ETH. Liquidity risk was arguably already offset by the secondary market where holders of staked tokens can trade them for ETH on decentralized exchanges. However, staked tokens continuously trade at a discount and the peg has historically worsened in periods of market distress. Lido’s LST, stETH, traded by as low as -7% relative to ETH after the collapse of Terra in June 2022 and -5% after the FTX fallout in November 2022. (See Figure 18)

Figure 18. Lido stETH to ETH ComparisonSource: CoinMarketCap

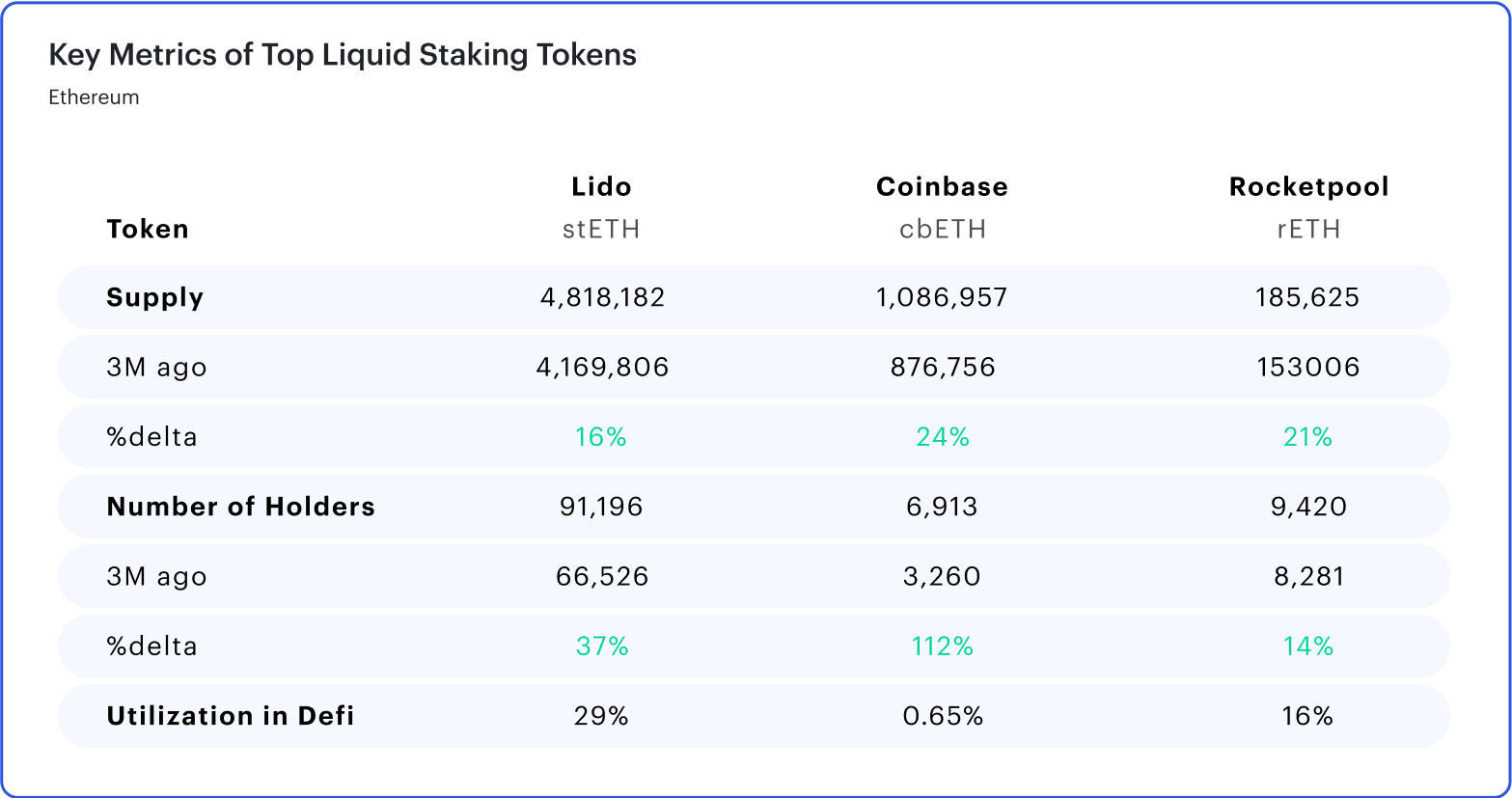

The ability to redeem staked tokens for the underlying ETH directly is a highly anticipated feature, even amongst those who have staked with a liquid staking protocol. Supply of staked tokens and the number of unique holders have increased across all top liquid staking providers in the last three months, with Lido increasing its number of stETH holders by 37%. Meanwhile, Coinbase offers a liquid staking solution through its centralised exchange and has seen the number of holders of its token, cbETH, more than double over that same time period. This indicates a large portion of non-native web3 participants are likely staking their ETH holdings ahead of the Shanghai/Capella upgrade. This trend also points to the fact that we may see increased market segmentation for providers, as new users with various degrees of expertise and risk profiles begin participating in staking.

Figure 19. Key Metrics of Top Liquid Staking Tokens (ETH)Source: Consensys, Nansen

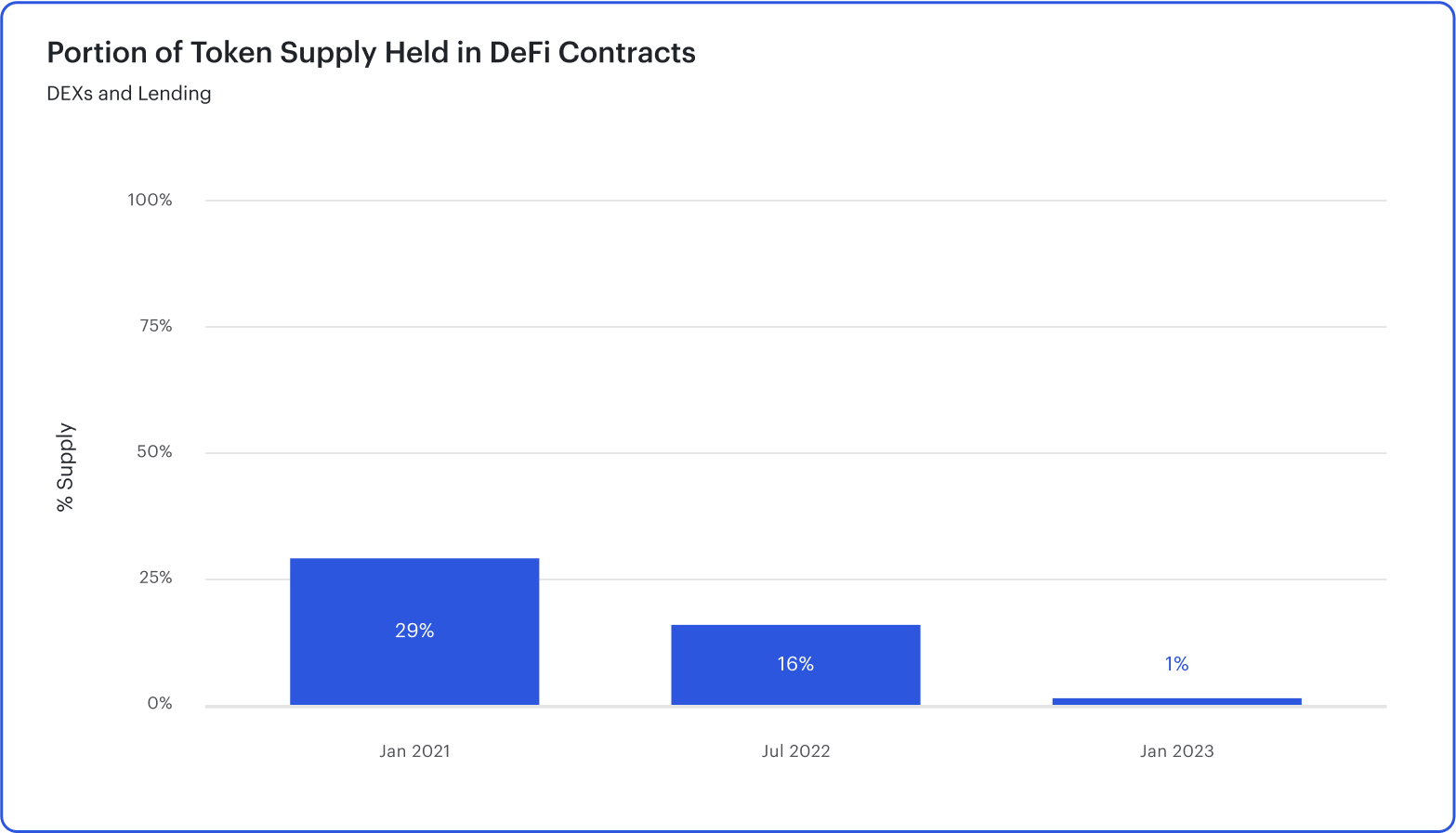

Finally, we expect to see an increased flow of staked ETH into DeFi protocols. The large majority of liquid staking tokens are not currently utilized in DeFi, with 29% of stETH and just 0.65% of cbETH currently sitting across decentralised exchanges and lending pools. The reason is likely related to the increased risk of depositing the LSTs for additional rewards across protocols. For example, lending against stETH is subject to the price risk of stETH/ETH, which can be volatile and expose users to liquidation. A more secure redemption of liquid staking tokens for ETH after the Shanghai/Capella upgrade will likely lead to more utilization across DeFi.

Figure 20. Supply of LSTs Held in DeFi ContractsSource: Consenys, Nansen

The disparity between DeFi usage of Lido, Coinbase, and Rocket Pool’s LSTs is likely a function of their degree of integration in the ecosystem. Lido has established itself as a leader in liquid staking and its stETH token is supported by more protocols than both cbETH and rETH. But as usage across LSTs increases, we will likely have protocols supporting a wider range of these tokens, which subsequently opens the door to higher volumes and overall growth of the ecosystem.

Join us for a discussion on how the Ethereum landscape will evolve following the Shanghai/Capella upgrade, and what that means for users. Watch the on-demand webinar →

The Shanghai/Capella Upgrade and Consensys

In the sections above, we looked at the technical details of the withdrawals process, the implications of withdrawals for the ETH staking market, and on DeFi. Now we focus on what the Shanghai/Capella upgrade means for the stakers, depending on where they are in their staking journeys and which service(s) they are using.

MetaMask

If you are a MetaMask user, you can stake ETH through MetaMask with liquid staking providers, Lido and RocketPool. Once withdrawals are enabled, you will be able to withdraw the ETH you have staked with these providers, irrespective of whether you have staked with them directly, or via MetaMask.

MetaMask will support withdrawals for Lido and RocketPool as soon as these services finalize their specs and enable withdrawals. If you withdraw directly from Lido or RocketPool, it will likely involve some delay between requesting a withdrawal and getting your ETH back. MetaMask users can get their ETH quicker by swapping their tokens – stETH for Lido and rETH for RocketPool – via a swap.

In this post-Merge world, there is a growing demand for simple staking services that will ultimately secure Ethereum. MetaMask Staking offers everyone an intuitive way to jump in and stake your ETH for rewards.

Learn more about MetaMask Staking →

Consensys Staking

If you are staking with Consensys Staking, either through the user interface or the API, you will be able to withdraw your staked ETH after the protocol upgrade. Users who have accumulated Consensys Layer rewards on their validators will automatically receive the validator balances that exceed 32 ETH, as a result of the “skimming” operation (see the Partial Withdrawals section above for more details).

Once withdrawals are enabled, we anticipate more ETH holders will stake as the activity becomes less risky. With the ability to un-stake ETH, users that may have wanted to stake, but were worried about the lock-up, can now get involved. As such, we anticipate more ETH will be staked, and the Ethereum staking ratio will increase.

As per whether some stakers will switch from their current staking providers to others: We anticipate that stakers will evaluate their current provider according to historical security, reliability, reward performance, and fees.

Consensys Staking aims to enable everyone, everywhere to be able to stake in decentralized networks. We work towards this goal by providing the most reliable and secure staking solution, with easy-to-use staking experiences.

Learn more about Consensys Staking →

Besu & Teku

If you are a solo staker running your own validator, it is important to ensure that you test the withdrawals process before you initiate it on mainnet. There will be multiple opportunities for you to do this, in the form of testnets that the Core Devs will launch.

Before the hard fork upgrades, client teams, including those at Besu and Teku, will upgrade the Goerli and Sepolia testnets to support withdrawals. Once that happens, Besu and Teku will have releases ready where users will be able to test the withdrawals process on those networks. You will need testnet ETH and testnet validators to test on these networks.

An important thing to keep in mind is that only stakers with the 0x01 withdrawal credentials will be able to withdraw their ETH. Around 311K validators still have the old-style 0x00/BLS credentials and will need to send a message via their node to change to 0x01 before their withdrawals can happen. So make sure to check your withdrawal credentials before initiating the process.

On the Besu side, there are some minor EVM changes that smart contract developers need to be aware of.

If you are running the Besu and Teku clients, make sure to follow all communication about the releases from the teams on Twitter and Discord. Additionally, stakers wishing to test out the functionality should stay tuned to the EthStaker community and Ethereum Foundation (EF) announcements. The EF also hosts community calls to provide useful information on upcoming upgrades and changes. This is a great venue for stakers and users to directly ask questions of Core Devs.

How will Consensys’ staking-related products, and their users be impacted by the Shanghai/Capella upgrade? Watch the on-demand webinar where our experts break it down.

Conclusion

The Ethereum roadmap works towards developing the Ethereum blockchain as the foundation of our digital future. Last September, The Merge unified Ethereum’s execution and consensys layers, marking the completion of Ethereum’s transition to Proof of Stake. This upgrade brought stronger settlement finality guarantees, prepared the chain to enable sharding, and drastically reduced ETH issuance and energy consumption.

Soon, Shanghai/Capella will deliver withdrawals. In other words, it will enable ETH “locked” in validator balances on the consensys layer to be withdrawn, and credited to an Ethereum execution account. This upgrade represents a significant liquidity event for Ethereum, with implications for every staker, the liquid supply of ETH, the competitiveness of the Ethereum staking industry, and the pace of both business model and technological innovation in the Ethereum staking space.

The next planned upgrade to Ethereum is the Cancun-Deneb upgrade, expected to be delivered later in 2023. This upgrade will deliver EIP-4844, an important step towards scaling Ethereum. EIP-4844 introduces a new Ethereum transaction type that accepts “blobs” of data. It should scale Layer 2 rollups on Ethereum and help reduce the transaction fees incurred by the users of these scaling solutions.

The contents of future upgrades, and the order in which they’ll be performed, remain to be decided. However, as the Ethereum Core Devs become increasingly practiced at deploying testing infrastructure, and as more talented contributors enter the space, Ethereum’s rapid evolution should only continue to accelerate.

Want to learn more? Hear from experts on how the Shanghai/Capella upgrade furthers the importance of decentralization and the impacts on retail and institutional users. Watch the on-demand webinar →